NOTICE TO CLIENTS AND FRIENDS

Tax & Employee Benefits Department

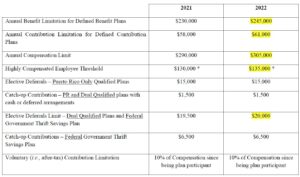

As required by Section 1081.01(h) of the Puerto Rico Internal Revenue Code of 2011, as amended (the “PR Code”), the Puerto Rico Treasury Department (“PR Treasury”) recently issued Circular Letter of Internal Revenue No.22-01 (“CL IR”) with the applicable 2022 dollar limits for Puerto Rico qualified retirement plans, following the recent announcement by the Internal Revenue Service (“IRS”) in IRS Notice with respect to United States tax qualified retirement plans. The Puerto Rico limitations are generally applicable to tax qualified plans under Section 1081.01 of the PR Code. Some of the key limits for tax years 2021 and 2022 are as follows with changes highlighted in yellow:

(*) This is the limit for the base year (2021 for year 2022 testing, and 2022 for 2023 testing) in the case of calendar year plans, as described in the principles in Circular Letter.

****

This document has been prepared for information purposes only and is not intended as and should not be relied upon as legal advice. If you have any questions or comments about the matters discussed in this notice, wish to obtain more information related thereto, or about its possible effect(s) on policy or operational matters, please contact us.